Building Your Nest Egg

Building Your Nest Egg

Understanding Asset Allocation

No. 6

As I have stated from the start, this newsletter is not and will not become another investment newsletter. However, I have received several requests from readers about how to get started with investing their hard-earned money and will do my best to provide some information about the places where you can begin to invest and the most important concept of all, asset diversification.

Simple ways to get started

Getting started investing is often the most intimidating step. There is so much information and advice floating around that doing nothing often becomes the most comfortable thing to do. Some recommend establishing a relationship with a full-service brokerage firm (e.g., Morgan Stanley, Goldman Sachs). However, to reap the benefits of the relationship you’ll need a significant amount of cash otherwise you are shuttled off to an online platform that they own. Also, brokerages make money by charging commissions on trades.

Another option is a discount broker (e.g., Charles Schwab, TD Ameritrade, Robinhood). Typically accessed online, many of these firms offer tools to help you make investment decisions and have significantly lowered or eliminated the commissions that they charge. Some are now even offering personalized service.

Similar to discount brokers are investment and mutual fund companies (e.g., Fidelity, Vanguard). They also have investment tools and some personalized services. The major difference is that they offer access to mutual funds and ETFs that they manage directly. They make money primarily through fees charged on the capital you have invested with them.

Last are money managers, or individuals who offer a more personalized investment, and planning advice. They can hand hold you through goal setting, investment planning, and investment management. In general, you’ll again need a large sum of money to get their attention and pay fees for planning and management.

If you are just starting out and don’t have a large enough amount of capital to get you personalized advice, it’s best to start with a discount broker or mutual fund company. The primary objectives at this point are to save on fees (more on this later) and pick a service that gives you the best level of comfort with the tools and advice for planning provided.

Asset Allocation and Risk

The next task is to figure out where to invest or allocate your cash. This is where the portfolio theory of diversification comes into focus. Perhaps you’ve heard the expression, “Never put all your eggs in one basket.” Well, it’s the same for dollars invested. If all your money is in one thing, then it may not be as safe as you think. Diversification allows you to spread risk across several asset classes that are preferably non-correlating, which means that when one asset goes up, the other may go down.

Don’t be intimidated by asset allocation. Most investment platforms offer tools that allow you to create a well-balanced portfolio based upon risk tolerance, goals, and your age.

But before we go much further let’s look at the types of assets that can make up your portfolio.

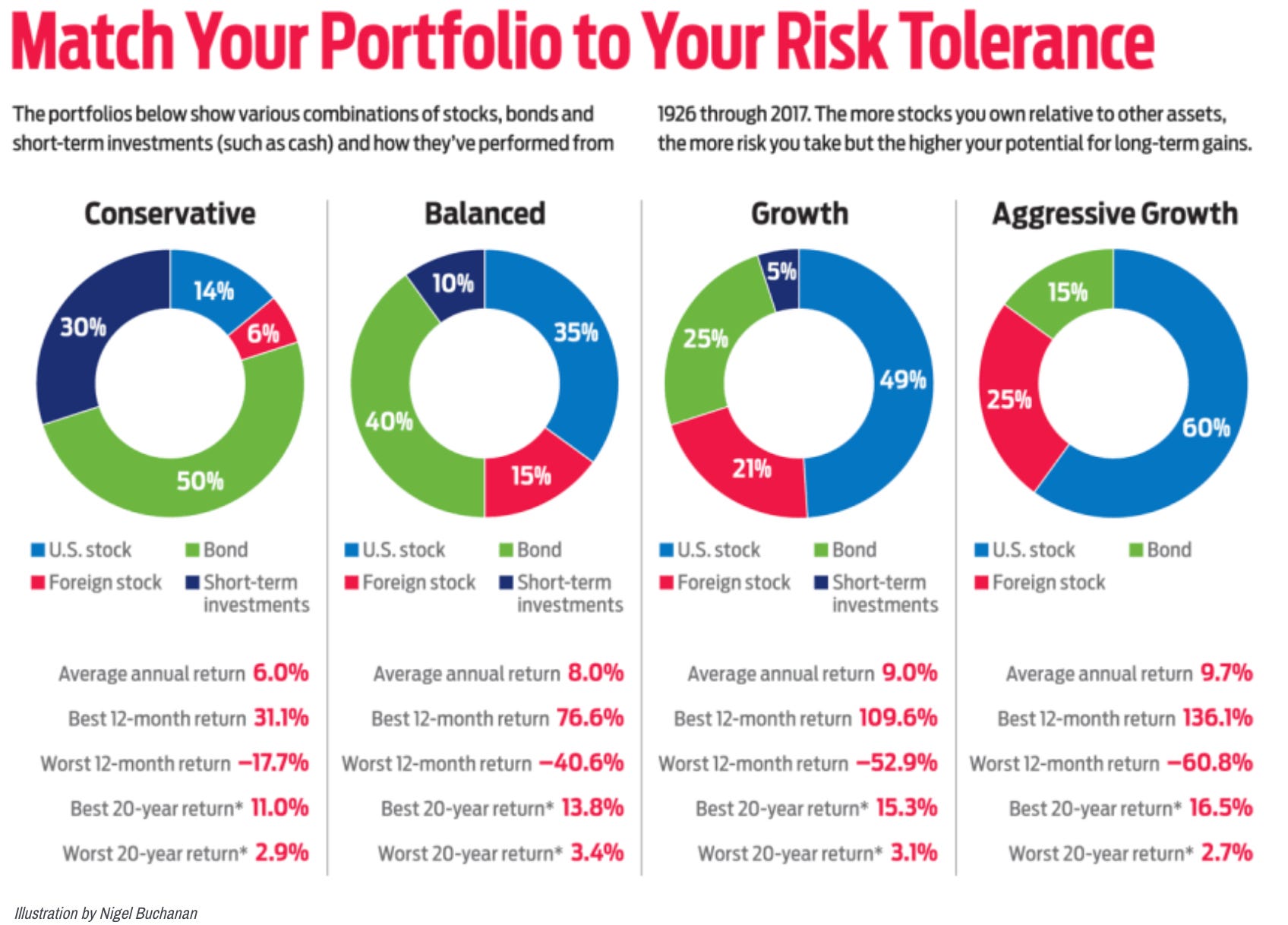

How you allocate your assets should depend upon your short-term and long-term goals as well as your tolerance for risk. Risk is often affected by your age as well as your ability to handle market fluctuations financially and emotionally. For example, if you are in your twenties and building a portfolio with the hope of taking retirement in your sixties, you might be willing to take more risk now and deal with the ups and downs of the market in the hope of getting higher returns. Therefore, your asset allocation might look like the ”Growth” or “Aggressive Growth” portfolios below. However, as you get closer to retirement age, your tolerance for risk might wane, because significant market downturn would mean changing your retirement plans. In this case, your asset allocation might look like the “Conservative” or “Balanced” portfolios below.

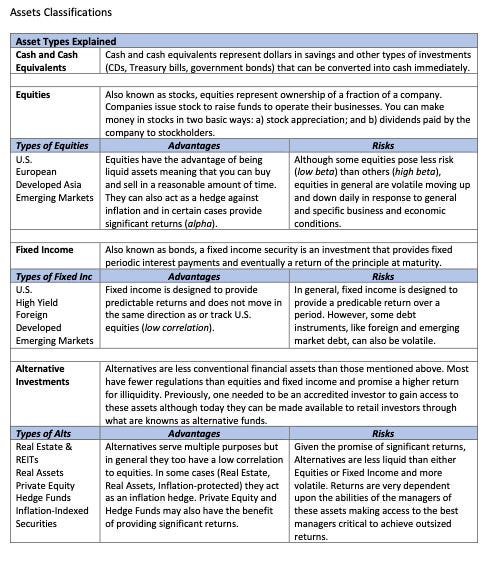

Think of your portfolio as a basket of items that you are purchasing for a journey in which you need to be ready for anything. The basket has various asset types (Cash, Equities, Fixed Income, Alternatives) providing diversity in terms of liquidity, correlation, risk, and return. You can further diversify within each asset class. For instance, you might have Domestic and Foreign Equities. And within those you might have Large Cap, Mid Cap and Small Cap Equities that represent businesses of different size and style or return expectations. The possibilities are endless, but the objective is simple – create a portfolio that provides returns in any market conditions.

The exhibits below provide a way to think about risk when considering investing in equities and fixed income. It is important to understand the risk that an individual stock, mutual fund, or ETF represents before investing. Equities are categorized by company size or capitalization. They are further categorized as value stocks (more stable performance), growth stocks (more volatile performance), or a blend of both.

When thinking about fixed income one must first consider the quality of the bonds, and second, the duration. The duration of the bond which influences interest rate sensitivity. The value of short-term bonds (e.g., maturity in >5 years) will be less sensitive to an increase in interest rates, while the value of long-term bonds may be highly sensitive to increases in interest rates.

You can work with one of the models above and build a portfolio designed to achieve your goals by investing in individual stocks, mutual funds, and ETFs. Many investment platforms will provide tools that recommend specific funds in which to invest. You can find an allocation that you are comfortable will meet your goals and pretty much stick with it through thick and thin. However, you may want to tweak your portfolio depending upon different market cycles. For instance, in a period of high inflation, you may want to have more assets allocated to real estate, hard assets or commodities, and inflation-protected securities. Whether you hold course and not make changes or try to adjust your portfolio to market conditions these moves should be tweaks, rather than wholesale shifts in your portfolio. If you try to time the market, you will likely end up chasing it and buying and selling at the exact wrong times, almost always resulting in value destruction.

Taxes and Fees

Taxes and fees erode your returns. Think of your portfolio as a bucket and each year you want to see the bucket fill with more water that represents value to you. Taxes and fees are a small hole in the bucket that leaks out never to be seen again.

Taxes are somewhat unavoidable, but if you are someone who likes to constantly buy and sell assets, you will incur taxes now rather than in the future. Fees can and should be avoided or at least minimized. There are many ways that financial institutions and professionals can eat away at your hard-earned gains through hidden fees and transaction costs. Make sure you understand all costs associated with an investment before making a commitment and do not invest in what you don’t understand.

If you really want to keep it really simple, then just purchase Index Funds (ETFs). These are baskets of the entire stock market, or sectors of the market, and are cheap and easy to understand. More importantly you pay very low fees, very low transaction cost, and they are very tax efficient. So, perhaps the easiest thing to do is diversify using stock and bond Index funds and simply leave it alone.

This is a start. If you have further questions please leave a comment and I’ll do my best to answer. Also feel free to suggest further topics to be covered in the future.