Buy Now, Pain Later

No. 13

Why read?

Learn about Buy Now, Pay Later

Compare BNPL to Credit Cards

Read about how to prepare for the impact of inflation

Check out my online courses for entrepreneurs

By now you’ve probably heard of or even used BNPL (Buy Now, Pay Later) offers from your credit card company or firms like, Affirm, Klarna, Sezzle, and Zip, but have you bothered to read the fine print? Do you know if BNPL is better than just carrying a balance on your credit card? Should you carry a balance on your credit card? Should you bother to use BNPL?

What is Buy Now, Pay Later?

BNLP companies promised a credit revolution that would change the way people purchase goods. BNPL is essentially a loan at the point-of-sale that allows you to split up the cost of your purchase into installment payments that are typically due every two weeks and without interest payments. Much of the time you’ll see BNPL offers on ecommerce sites, but providers are now offering cards that you can use when not shopping online. Aren’t they kind?

How does BNPL work?

So, you see that new pair of shoes that you really covet and just must buy them now but don’t have the cash. You can use BNPL to pick up those kicks before the store runs out of your size and just make 4 easy payments over the next 6 weeks! Sounds too good to be true.

Why stop at the shoes? How about that 60-inch 4K TV? Oh wait, 4 payments are still steep. Whaaat? I can take up to 12 months to pay if I just accept some interest payments. Huzzah! I love American consumerism!

Hold on a minute. The interest rate is 39.9% APR. Let that sink in. You’re almost buying the TV twice. And about those shoes you purchased using BNPL. Don’t miss a payment because some of these providers will hit you with a settlement fee or a lump sum interest payment that is added to the amount you already owe. But wait there’s more. You get charged a late fee too and congratulations you have also affected your credit score. There’s good news, sort of. If you already have a poor credit score you are likely not eligible for BNPL.

Credit Card vs. BNPL: The Good, The Bad, & The Ugly

The lines between credit cards and BNPL plans are beginning to blur making it more challenging to determine which is better to use. Some credit card companies are offering BNPL plans for some purchases and some BNPL companies are offering credit cards.

Credit cards:

You first must apply for one and have good enough credit and income to receive a card

Once you have a card you can use it to make purchases until you hit your credit limit

Credit cards charge annual fees, usage fees, and have high interest rates

Each month you can either pay down the entire amount owed or make the minimum required payment ($25 - $35) and carry a balance for which you are charged interest. However, if you choose to only make minimum payments you may never pay off your card in full depending upon the interest rate charged

Credit cards do offer some benefits such as, travel rewards, purchase protection, and insurance on purchases

Credit card issuers report to all three credit bureaus regularly

BNPL:

You have the option of applying for a BNPL plan or card ahead of time, or simply use the offer at the point-of-sale

Given your credit score you may be denied from using BNPL, or have limits on the amount that you can loan

Purchases are typically split into 4 equal payments – 1 at the time of purchase and 3 additional payments that are due every two weeks. Plans that offer longer payback periods may charge high interest

BNPL generally do not charge fees or interest. However, if you miss a payment, you will be charged both fees and very high interest that is added to your loan amount

BNPL plans don’t come with the same types of benefits offered by credit cards, nor do they offer purchase protection plans and might also make returns more difficult

BNPL companies do not report to credit bureaus regularly but do report any past due amounts. In other words, BNPL can’t help you build good credit, but can damage to your credit if you make a late payment

Which is better?

It depends. If you have a credit card and you pay your balance monthly, you are taking advantage of the float (the time between purchasing and when payment is due) and not paying any interest. However, if you don’t have a credit card then a BNPL may be of use if you are certain that you can make every payment on time.

The Bottom Line – If you don’t have the cash to buy it then wait until you do. And when you have the cash to buy it make sure you can afford it. What I mean is that some things come with ongoing costs (subscriptions, taxes, insurance, maintenance) and you must budget for these monthly expenses before you decide to make a purchase. Credit cards and BNPL plans make buying easier but used incorrectly you run the risk of accumulating large debts and do damage to your credit rating. So, use with an abundance of caution.

If you received this from a friend consider your own FREE subscription.

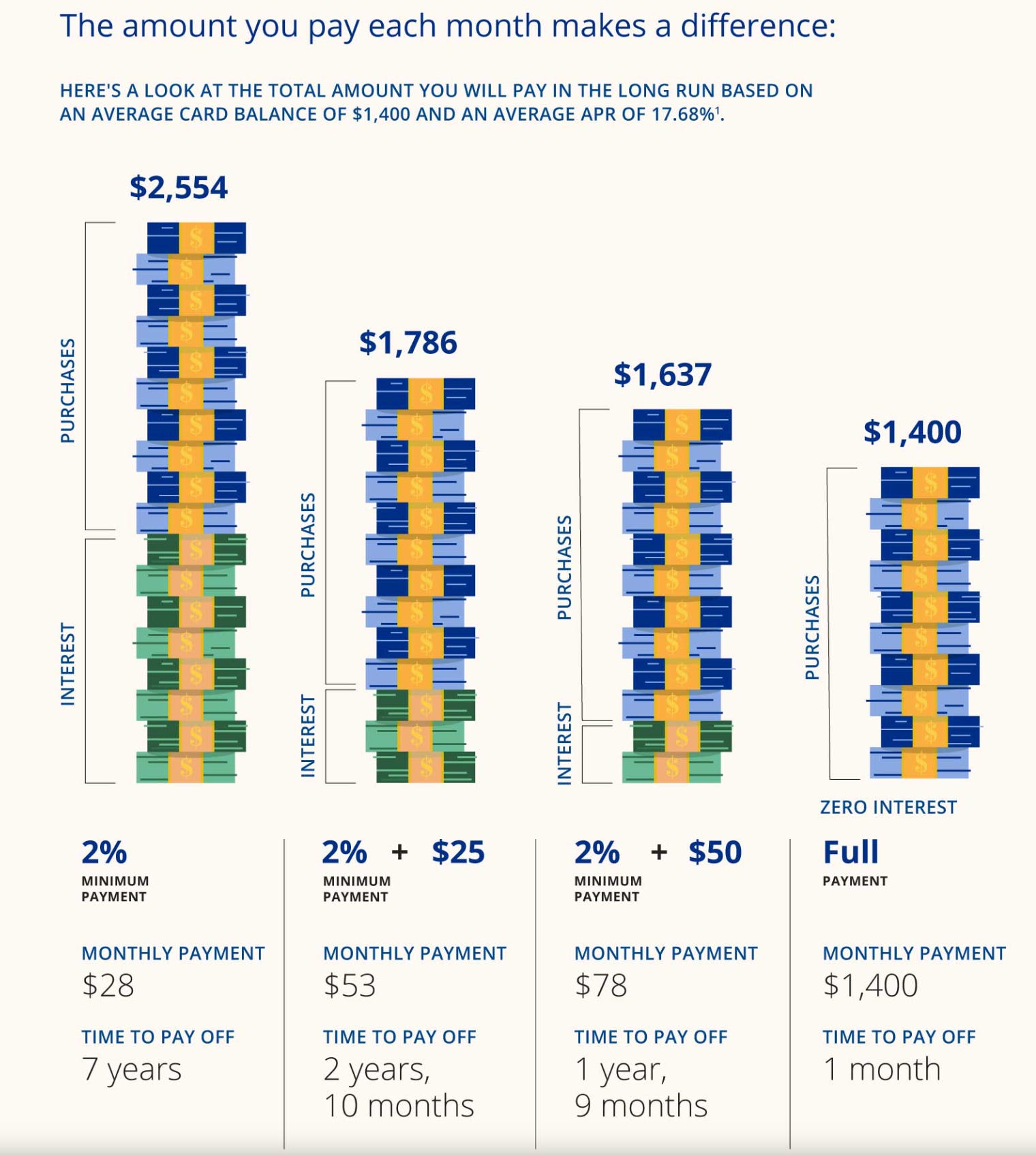

One Chart

I found this while doing research on BNPL and though it related to credit cards and APR it also applies to any debt.

The Markets, Recession, and Inflation

In my first post I made it clear that I would not be dispensing investment advice. That said, I am constantly asked about my thoughts on the markets and economy so here are a few short answers.

Q: What will the stock market do?

A: Fluctuate

Q: Will we go into recession?

A: Yes, recessions happen. They are a normal occurrence.

Q: When?

A: I don’t know. Most economists don’t know that we are in a recession until we’ve been in one for a quarter or two. What do I look like a fortune teller?

A: What about it? It’s here and may be here for a while.

The Fed is doing its best to attempt to control it without throwing the country into recession, which is as likely as running through a river and not getting wet. Essentially, the Fed will raise rates which will make the cost of capital more expensive. This should slow the economy down just enough to get more equilibrium between supply and demand of goods and services which should result in less price inflation. However, if demand slows too much the economy can be pushed into a recession. The big fear is an Ursus Magnus that rivals the economy of the 70s. (FYI the Dow Jones dropped from a high of 6,939.20 in December 1972 to a low of 2,297.50 in July 1982. That’s a -65.5% drop in 10 years) Let’s hope it doesn’t come to that.

Inflation is a thief. It robs you while you’re awake and asleep. Everything is more expensive, not just gas but entertainment, food, and rent to name a few. If you don’t have a handle on your budget, now is the time to do so. Try to curb your spending habits and find ways to honor your values without dropping big bucks. Consider new ways to save money on groceries and gas. It would be very wise to have 3 to 6 months of expense cash in the bank should we dip into recession, and you find yourself between jobs.

“Despite the high cost of living it remains popular.”

Educational Offerings:

Check out my online courses for entrepreneurs at Entrepreneurial-Edge

Founder Finance - Finance for non-financial people who want to build a startup

ETA: Buying a Small Business - Everything you need to know to find, negotiate, and buy a business for yourself

Business Model Innovation - A time tested method for evaluating or creating business models

FREE Getting from Seed to Series A - Learn how to raise capital for your startup

Further Reading on BNPL:

Excellent as always. Love the metaphor of running through the river :-)

Excellent as always. Love the metaphor of running through the river :-)